A Guide to Building Reasonable Startup Financial Projections

Essential skills for entrepreneurs.

Introduction

Financial planning and analysis are critical skills for entrepreneurs to develop. To assess the viability of a business venture and communicate its economic prospects, founders must learn how to prepare critical financial statements. This article combines three essential topics related to startup financial statements: revenue forecasts, cost estimates, and pro forma statements.

Revenue forecasts require careful thought into pricing, sales cycles, customer acquisition, and growth rates. Documenting assumptions and outlining the sales process sets the foundation for credible top-line projections. Cost estimates keep entrepreneurs grounded in the required expenses to operate their business model, from pre-launch outlays to ongoing overhead. Finally, pro forma financial statements combine these projections into integrated documents that allow analysis of profitability, cash flow, and financial position.

Mastering financial statement preparation positions founders to evaluate their business model, communicate with stakeholders, and monitor performance. However, entrepreneurs must remain nimble and adapt as new information emerges post-launch. The combined insights in this article aim to provide a comprehensive overview of building, integrating, and using financial statements to increase the odds of startup success.

This article aims to provide startup founders with a solid grounding across three core financial planning and analysis aspects. By the end, readers will understand how to thoroughly build out revenue forecasts, diligently estimate costs, and accurately prepare pro forma financial statements. This knowledge equips entrepreneurs with essential skills to quantify their business model, evaluate viability, communicate with stakeholders, and monitor performance. Developing proficiency in financial statement preparation will enable founders to make smarter decisions in pursuing startup success. With a dedication to financial rigor in the early stages, founders give their ventures the best shot at prosperity.

The Challenge of Startup Financial Planning

Crafting financial projections for a new business comes with inherent challenges. With no historical data to reference, founders must make assumptions and estimates across all statement elements. Estimating revenues and costs without existing customers requires researching target segments, the competitive landscape, and industry benchmarks. Founders may lack access to reliable market data, particularly for innovative products. They must avoid inherent optimism bias when assessing demand and growth potential.

Entrepreneurial Forecasting: Strategies for Making Informed Financial Assumptions and Avoiding Common Pitfalls

Hi Innovate and Thrive Subscribers! When you participate in Irrational Labs'Behavioral Economics Bootcamp, you join a thriving community with fantastic access to behavioral scientists through virtual webinars, special reports, and a very active Slack community. Read the sidebar in this post on Artificial Intelligence's role in financial planning based on a recent whitepaper,

On the operational side, anticipating required investments and expenses involves much guesswork. Founders may underestimate the salaries needed to acquire top talent or the costs of R&D and product testing. Unforeseen costs always emerge pre-launch and post-launch. Additionally, founders struggle to integrate statement elements across revenue forecasts, cost estimates, and cash flows. Ensuring smooth connections between statements is imperative for accurate planning. With a dedication to continuous research, founders can create reasonable projections while remaining agile to modify based on real-world data.

As with many venture realization activities, I always try to make the steps as simple as possible for founders. Creating a new enterprise from scratch requires searching for a great deal of further information about the problem to be solved, your target customer, and the marketplace. And if this is not enough, you are challenged to create a business model and translate it into a robust set of financial statements.

Startup financial projections are important as they reflect the underlying business model in a standard quantitative language that all stakeholders can understand. Creating these financial projections requires founders to consider each element of their business model in an internally consistent manner. I think of it as a transaction between the venture and the customer, looking at each relationship aspect translated in quantitative terms. It facilitates an understanding of the feasibility of the business model in terms of its repeatability and sustainability. Detailed financial modeling allows the founder to assess the strengths and improvement areas of the venture's business model.

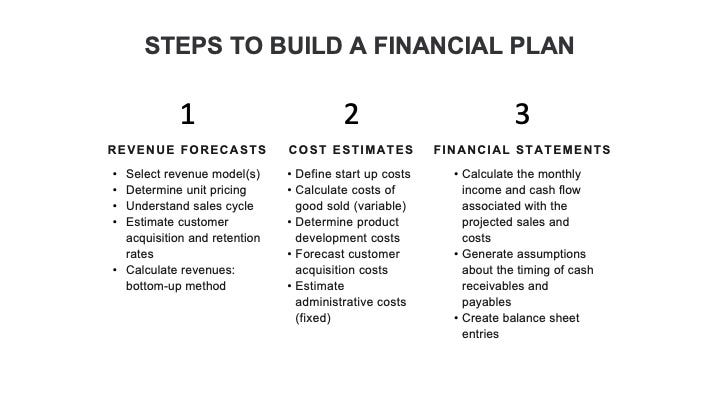

Three Basic Steps

I break the basic steps to building robust startup financial projections into three stages: revenue forecasts, cost estimates, and pro-forma financial statements. Several elements require research, assumptions, and underlying estimations with each step. So let's work through each step and essential elements.

Step 1: Revenue Forecasts

I suggest that founders start the planning process by tackling what many consider the most challenging aspect of startup financial planning - the sales forecast. In other words, estimating the amount of sales dollars your business model generates each month over a specified period.

You make several decisions before you can forecast your venture's revenues. These include selected revenue models, sales cycles, pricing, customer acquisition rates, and operational capacity. As you will see, you need all this information to conduct a bottom-up analysis for your revenue projections.

From experience, estimating anticipated revenues for a new business is highly challenging. So, it is understandable that these early forecasts are fraught with problems. However, founders can mitigate these challenges in revenue forecasting by solid due diligence about the customer's purchasing behavior, including how long it takes to decide to buy a product from initial interest.

Your sales forecasts should take several things into account. These include: how your marketing strategy will drive customers to your business, the typical conversion rate from customer interest to the actual purchase, the efficacy of your distribution channels, and customer acceptance of price based on the value placed on a solution. Without this understanding, you can easily underestimate the time it takes to generate revenues or overestimate the pace of customer acquisition and sales.

It is important to remember that your revenue models will change and probably expand as your business grows. Successful ventures rarely stick with one revenue model without modification or expanding to multiple revenue streams. For example, many e-commerce ventures begin revenues directly from the sales of their products. The web presence will become more attractive for potential third-party advertisers, affiliate programs, and e-mail list rentals as their customers grow. Founders are encouraged to think ahead about how their revenue models will change and encourage them to consider how these changes will affect future financial outcomes.

When you are ready to start building the revenue side of your financial model, you can follow these five steps. First, discuss your revenue model and pricing strategies, then research outlining the sales transaction process in detail and ascertaining benchmarks for customer acquisition and retention rates. Then, you should have enough information to build a monthly revenue forecast.

Select revenue model

Determine pricing strategies.

Visualize the sales process and sales cycle.

Estimate customer acquisition and retention rates.

Calculate revenues: bottom-up method.

Revenue Model Selection

Let's start with selecting the revenue model that best fits your product and customer. There are many considerations when choosing what the transaction between your business and the customer will look like. First, you want to determine your customer's current purchase behavior related to existing solutions as a starting point. As stated in earlier posts, you can evaluate customers' current behavior during customer discovery. What do they do now, and what are they used to regarding similar products? Market research will also provide important information about what competitors currently apply revenue models.

Revenue models come in many forms, from traditional transactions, such as paying a one-time charge for a product or service, to digital transactions, such as a monthly or annual subscription to a software application. As stated above, your choice of revenue model will depend on several circumstances, and your eventual selection will significantly rely on the customer's current purchasing behavior and standard practices in the marketplace. In the worksheet below, you will find many common categories of revenue model transactions. But founders should not just check a box. Instead, you may choose several models or a hybrid of transactional approaches. For example, you may charge a one-time, upfront fee for a product and then provide payment options for additional services, extended maintenance, or warranties.

While there are several revenue models, don't be afraid to innovate. Creating a new or hybrid revenue model can differentiate your offer from what is currently in the marketplace. In addition, testing a new approach during early market testing can help validate if the customer finds the model attractive and of better value than the competition.

Pricing Decisions

You should determine your pricing strategy in conjunction with selecting your revenue model. How much will you charge the customer for your product and service? Additionally, how will the customer pay, and within what time frame? Will they pay the whole amount at the time of the transaction? Or will customers be able to pay over a certain period? For a software product, will the subscription be monthly or annual? Will they get a discount if they pay upfront instead of monthly?

As you start considering various pricing strategies, you must consider what value customers will derive from your product. Startups must stay focused on the value they provide to the customer no matter what other objectives they hope to achieve through pricing. You are trying to accomplish different goals through pricing. For most startups, the primary aim is reaching breakeven and becoming cash-flow positive. Customer acquisition rates may often be key if you engage with outside investors. If you offer something new, you will want to build market share quickly to be first to market. The business objectives may vary, but customer value is always the priority. Your final pricing decisions are driven by what the customer is willing to pay based on perceived value.

As a starting point, startups want to balance two pricing methods - Cost-plus and value-based pricing. The cost-plus approach is determined by considering the costs to produce your product and then adding a sufficient margin to offset fixed costs. I encourage knowing your unit economics. Startups must understand how much an individual transaction contributes to the venture's profits. Focusing solely on product costs for determining price is a significant mistake. The principal argument against this approach is that it leaves the customer out of the equation.

Value-based pricing is more challenging, but the process necessary to calculate it is priceless. The process begins by quantifying the value you are providing to the customer. Once you determine the dollar amount of the customers' gains, you will charge a certain percentage of the value amount. How do you come up with the value amount? During customer discovery and MVP testing, you have many opportunities to assess the value while engaging your customers. For example, you should be inquiring how much they believe they are saving using your product during these engagement points. In a B2B context, you want to learn how much the enterprise values your solution. They will be looking for at least a 5X to 10X return. If they pay $100 for your service and it enables them to sell $1000 of product to their customer, you know you have provided good value to the enterprise. The customer's perceived value will determine how much risk they are taking upfront. For example, offering a subscription with cancellation provides less risk than paying the annual cost upfront.

There are other methods to determine the value placed on your offer by the customer. Your market research into available options in the marketplace will provide important comparative information. Learning how customers currently pay for solutions is a critical data point. In conjunction with this knowledge, understanding the degree of satisfaction with current options will add to your understanding of the value difference between your product and existing solutions.

Another factor in the value calculation is determining what different customer segments are willing to pay. Many founders are surprised to hear they can have different pricing strategies for different segments. While it takes research to learn these differences as you enter the marketplace, one segment is willing to pay more. Your primary target customer, the one you know who needs a solution and is extremely unhappy with all options, will be ready to pay a higher price. Your early enthusiasts and adopters are less sensitive to price because of need or passion. These early customers will help you determine the value of your offer while you continue to build and test your products. They can give you the traction to move towards more significant segments, where pricing sensitively increases, as does your marketing efforts.

Determining Sales Process | Sales cycle

Another critical step related to revenue and sales projections is determining the sales process and cycle. It is vital to map out your sales process and determine how long it takes from when you first engage a customer until the purchase is final. Start when the customer first becomes aware of your product as a solution to their problem. From this first awareness, how long does the customer gather enough information to buy the product? Finally, how is the final sale made, and how is the payment collected?

This step is crucial for B2B enterprises. As discussed in my post on B2B customer discovery, there is much to consider to ensure you understand what it takes to complete a successful sales process. For example, I recently consulted with a B2B enterprise whose primary customers are large global corporations. In these corporations, every division had its own set of decision-makers and procurement processes, each with a different number of steps and timelines. One of the first things they did was build out a detailed step-by-step sales process. Then, we looked at each step in detail, examining how we could expedite the sales process, shorten the life cycle, and increase revenues. For example, one of the significant steps in the sales cycle was establishing a trial period where the customer would receive a free product for testing. By isolating a specific phase, we could brainstorm optional ways to expedite trial periods or charge for more extended trial periods. These ideas arise when you dissect the sales process, looking for new ways to deliver value to the customer while improving your business model.

From a forecasting point of view, founders need to know how long each sales process step takes to estimate the timing between marketing activities, booked sales, to payment. This information allows you to make credible estimates of how much new customers cost to acquire, when sales are acknowledged, and when payment will occur. Knowing when to expect payment is critical to projecting and managing cash flow.

Estimate Customer Acquisition & Retention Rates

The next task in your sales forecasting activity is to estimate the customer acquisition rate and, if applicable, retention rates. You must consider several factors to determine better the speed and cost of acquiring new customers. Understanding the sales cycle length includes understanding if the decision-maker differs from the user, the time from decision to purchase, and identifying potential obstacles that inhibit sales or payment.

Based on your understanding of the customer's full-cycle usage of the product, you should be able to answer such questions as how customers determine that they need/want to purchase your product (change from the existing solution). How do customers find out about your product? How do they acquire your product? How will they pay for your product?

To estimate your customer acquisition rates, determine how many customers you need to hit your revenue goal. Next, calculate the revenue goal divided by average sales per customer for a specified period. Once you know how many customers you need to reach your revenue target, you can calculate how many potential customers you need to get via your marketing channels. Finally, by applying what is commonly called "sales funnel math," you can estimate each sales channel. How many qualified leads do you need to achieve your sales goals? Necessary: Research the sales funnel conversion rates applicable to your industry, market, and product area.

Once you have determined how many customers you can acquire per marketing channel, you should create a promotional calendar, month by month. Along with your knowledge of the sales process, you can project a campaign's impact on sales and when the transactions occur. Estimating the effect and timing of a marketing campaign comes with its challenges. You must create opportunities to experiment and test promotional channels during minimal viable product iterations.

While you are thinking about the impact that marketing has on customer acquisition, you should also consider any factors that influence customer retention. Customer retention can be essential to your success, depending on your revenue model. For example, if you offer your customers a monthly subscription model, you can expect attrition throughout the year. Sometimes, you may be able to gather some early attrition data during customer discovery and product testing. Here is an excellent opportunity to apply industry retention benchmarks to your financial model.

Applying the Bottom-Up Method

There are two ways to approach revenue projections, top-down versus bottom-up. While I highly encourage you to analyze the bottom up, there is value in doing both.

The top-down analysis builds on market size and demand estimates. As discussed in an earlier post, you begin to determine the size of your market with a focus on your primary target customer segment. Your central emphasis will be on your served available market (SAM). The SAM is the number of potential target customers that meet the demographics and behavioral characteristics demonstrating their intense interest in having your solution combined with a deep dissatisfaction with current options. The top-down method adds value when the target market is well-defined. This approach proves less valuable if the market is fragmented or in the early stage of adopting a particular innovation.

The startup can begin to develop its go-to-market strategy to capture a portion of the SAM from this point. The capture rate or market share (SOM) will depend on several factors, including the marketing plans' efficacy and the venture's operational capacity. The transition from SAM to SOM is where you shift your analytic approach to bottom-up. The bottom-up approach asks the founders to realistically estimate how much product they can produce and sell during a given period.

The starting point for a bottom-up analysis is the definition of each sales unit. Some new ventures start with only one product to develop and sell. This situation makes the analysis more straightforward (though no less challenging). When will the product development be completed? What is the timing and capacity to produce the product? What is the promotional calendar and sales cycle? Answers to these questions will help determine the number of units sold daily, monthly, and annually.

Each revenue source should have its line in the income statement. There are many reasons for this practice. Each product will most likely have different pricing & discount strategies, costs of goods sold, launch dates, and growth rates. All these variables make estimating sales all the more challenging.

Determining growth rates is one of the more difficult factors to estimate. For this reason, one typically sees founders falling back on top-down estimates by using industry benchmarks to apply growth percentages to product sales. Unfortunately, this method does not consider your marketing plans or capacity to achieve this growth. Therefore, it is essential to identify your revenue drivers and do your best to invalidate the assumptions and estimates behind them.

Recently, funding for new ventures has stalled due to several economic factors ranging from rising interest rates to rapidly growing inflation. As a result, many significantly funded startups with historically high valuations are not meeting growth targets. Additionally, they are experiencing unanticipated rising costs. Suddenly, it's time for startups to embrace frugality and focus on breaking even, the gist of the founders quoted in the article.

A startup should always exercise financial discipline, a practice beginning from the earliest stage of development. As I work on this startup finance series, it is clear how vital the economic field is for the founders to embrace early.

Step 2: Cost Estimates

For a new venture, we break up the essential cost elements into startup costs, costs of goods sold, product development costs, customer acquisition costs, and other general administrative expenses required to operate the venture. Several cost estimates can be straightforward, such as specific startup or fixed administrative costs that you can quickly look up purchase details. For example, if you need a computer for your business, you can decide which one you need and research the best price to buy or lease it. However, some of the costs, especially variable expenses such as costs of goods sold and customer acquisition costs, are more challenging to estimate. This post will focus on startup costs incurred before opening for business.

Startup Costs

Startup costs are expenses incurred before you officially launch your business for revenue generation. In my experience, most founders underestimate the potential resources required to build a business plan and prepare for subsequent market entry. Every company will have its own unique set of requirements to prepare for market entry. Ventures that require physical assets such as brick-and-mortar locations, large starting inventories, or extensive research and development activities will face significant resource needs and associated expenditures. Other ventures can navigate the pre-launch phase with minimal costs. In either case, planning for financial needs pre-launch facilitates a vital leadership discipline that serves founders well throughout the journey.

As you prepare to brainstorm all potential startup costs, you should consider categorizing them in various ways. First, you should remember that some costs count as "expenses" and others as "assets" acquired before the business opens. Additionally, you want to separately record startup assets (required to launch) and expenses for accounting purposes.

There are implications for taxes and potential ownership equity discussions. For example, expenses may be tax-deductible in the current year, while the purchase of assets may be accounted for differently. So it is worth planning for and properly documenting these different transactions. The IRS guides founders on how to account for startup costs. Founders should make these decisions with advice from a certified public accountant.

It is also vital to divide it into one-time charges versus recurring expenses. Thinking about startup expenses helps founders plan for immediate versus longer-term cash needs. As part of your early financial planning, you will also consider how much cash is required as you open for business.

You can start this process by brainstorming all the items you will need before being able to implement your business model. Let's begin with startup assets.

Startup Assets

The costs of startup assets are commonly tangible items acquired before launching your venture. Before launching your venture, the amount you should spend depends on the business. In some cases, there is a need for extensive capital expenditures, usually associated with either physical assets or product development.

You can subdivide startup assets into these categories:

Physical assets that pertain to land, buildings, leasehold improvements required to ready business space before launch, office furniture, store fixtures & signage.

Tangible assets pertain to manufacturing, such as the plant, machinery, and other equipment necessary for production.

Inventory-related assets, including starting product items and raw materials.

Essential vehicles such as trucks and automobiles

Office equipment and computers

Intellectual property acquired before launch.

Founders can delay the purchase of certain physical assets while they perform product and market tests. For example, I have worked with food and beverage startups that aspire to open a brick-and-mortar establishment. While I encourage them to work on plans regarding location and space design, the critical path task items are getting the product in the hands of the customers for taste testing, packaging reviews, pricing sensitivities, and distribution channel selection. These early activities can be done via pop-ups in existing establishments, from small grocery stores to campus building lobbies.

One of my student founders recently wanted to establish a unique space for tutoring and learning. In the early stages, the founder focused on the location and the type of space aligned with the proposed strategic mission. The founder could find a place to host a test learning environment for a nominal fee by brainstorming options. However, the projected capital requirements to meet the long-term vision were relatively high, and it was essential first to establish the validity of the product offering with minimal expenses. In this case, the costs of running the pilot are considered deductible expenses and not assets. If renovation of a new location is eventually required, the founder can amortize much of the costs.

Inventory requirements can be another critical challenge for founders. To project without historical data, estimating how much inventory you need depends on several complex factors. Securing initial stock for marketplace entry can be challenging, depending on the product category. For example, physical technology products are typically expensive, from design effort through producing prototypes to actual manufacturing for inventory. Each element is costly.

Working with a team who envisioned an innovative countertop composting product, early development started with simple drawings and 3D renderings to illustrate the design and look of the product. This effort was followed by laying out the product's technical specifications to their ability. With technical specs, the next step is to approach manufacturing partners to validate design feasibility and provide estimated production costs. Once the founders validate that the design is workable and production costs are within the required margins, they can explore funding options like crowdfunding, corporate partnerships, and government funding pending the product to cover initial capital expenditures. Unfortunately, most startups never make it through all these phases before pivoting in another direction.

Consumer retail products are another category that typically requires inventory before the venture starts to generate revenues. Like other physical categories, consumer products must go through design - prototype - ready-to-sell phases, from fashion to food. Founders start with increasingly detailed designs for fashion items, usually culminating in tech packs. Tech packs contain detailed visual design sketches, required materials bills, and measurement specifications. With this information, founders, designers, and manufacturers can work together to create a cost sheet that includes materials and labor costs. This information will be the foundation of the startups' costs of goods sold estimates. The tech pack's cost depends on who drives the product design. I have worked with founders who designed their products and others who hired outside designers to create the final designs. Designers work in different ways, with some charging per hour while others charge a flat fee for a specific style. As a result, the cost can vary depending on the complexity of the design. From design to ready-to-sell inventory can be a costly proposition. Many consumer-driven products navigate some costs by applying a pre-selling model, whether via eCommerce sites or crowdfunding campaigns. These methods help to offset the initial pre-launch inventory costs.

You should be diligent about documenting any expenses related to starting inventory. Some elements of the early product preparation may be deductible as a startup expense as part of the current IRS cap of $5000. However, early inventory stock should be considered an asset, a balance sheet item. Once you start to sell products, the costs of producing the product will count as a cost of goods expense.

For startup assets, you should work with your accountant to decide which costs can be deductible in the current year under the $5000 cap and which may be amortized over a specific period. In the latter case, you will deduct a particular depreciation expense during each year of the amortization period.

Startup Expenses

You can break pre-startup expenses into the following areas:

Research and development costs

Fees such as installation fees, deposits, licenses, permits, legal fees, professional fees, insurance, office supplies

Pre-launch marketing materials, logo, brochures, website, and other promotional materials

Pre-operational training or labor costs

Additional miscellaneous costs specific to the nature of the business

Research and Development

This expense area that can be challenging for startups is the capital requirements for product development. Building early versions of the product requires extensive research and development for specific ventures. I cannot tell you how often founders despair over the forecasted costs of creating new technology. Sometimes, navigating the development costs can be tricky, especially when the hardware is involved. However, the founding team must plan development in cost-effective steps, whether it be software or hardware. Each stage focuses on increasing the fidelity of the product so you can build support for future innovation.

Typically R & D startup expenses may include:

Hardware and supplies to build your prototype.

Costs of leasing computers used for R&D activities.

Fees to third-party contractors to support early product development.

Founders working in specific technological areas may be eligible for a US Research & Experimentation Tax Credit that allows you to deduct these expenses up to $250,000 if your startup qualifies.

Legal Fees

I find the percentage of founders who try to avoid spending funds on legal fees interesting. Of course, frugal behavior is essential at some level's early stage of development. However, specific legal services are crucial to the startup's long-term viability.

Founders should consider three categories of legal services and associated expenses before launching - incorporation, founder agreements, and intellectual property protections. From experience, founders can find lawyers that offer a basic startup legal package that includes filings for incorporation, basic founder agreements, and confidentiality agreements that apply to various business relationships. Founders can procure these services for around USD 5K, not including local and state fees.

You will spend more if you plan to apply for a patent or register a trademark for intellectual property protection beyond basic confidentiality agreements. I have worked with many startups that have applied for provisional patent or trademark registration. Provisional patents help founders create a short-term placeholder for their intellectual property, providing an inexpensive and relatively quick way to establish first-to-file status. While it allows for relatively no protection, it gives you time to complete the more detailed non-provisional patent application. Trademark applications protect your venture's brand. Once you have decided on a company name and associated brand elements, it is worth doing due diligence early to ensure the name is not already protected. Provisional patents and trademark registration are two startup expenses well worth the investment.

Marketing & Branding

There is plenty of opportunities to spend on marketing and branding development during a startup's pre-launch period. Fees range from paying designers and brand consultants as founders find their way to unique brand identity. You may pay for the initial website design, marketing collateral materials, and associated printing costs. Some founders are responsible for creating their early brand identity, while others find it worthwhile to solicit professional advice. Some startups find a balance between the two approaches to keeping these essential costs down to a minimum. Several students have successfully developed their branding elements using designer marketplaces and crowdsourcing platforms. Additionally, founders have many template-driven sources to support website design and marketing materials.

Founders should set aside funds for experimenting with different promotional channels starting early in the venture development process. As I have mentioned in an earlier post, customer discovery and MVP iterations are optimal times to test and measure various marketing channels. Even small amounts such as USD 100 can provide insights into the effectiveness of a specific channel, such as Google or Facebook ads, for future customer acquisition strategies.

Customer acquisition costs are one of the most critical cost areas for new ventures. Typically, the marketing costs for a startup are one of the highest expenses, along with product development and human resources. One calculates Customer acquisition costs by determining all sales and marketing costs of acquiring a single average customer. Early experimentation and testing can ensure that founders spend these funds wisely.

Human Resources

Many startups have zealous, passionate founders who don't mind delaying compensating themselves until the enterprise is up and running. However, there are many situations when external experience and skillsets are needed, and compensation is required. In many cases, additional expertise is necessary for product development. Depending on the product category, you may need designers or software engineers. As mentioned earlier, I always push entrepreneurs to actively participate in their MVPs' early design and testing as their skill allows. At some point, you may need technical expertise beyond the team's capabilities. You can hire them as an early employee or as an independent contractor. In either case, these labor costs are inevitable.

There are times when founders may need specific education or training before operations. These are typically one-time costs but are essential to running the business. For example, a couple of years ago, a founder required certification to become a drone operator pilot for the future aerial photography business. Required funds included training and licensing. Most pre-launch training costs qualify as startup expenses. Generally, there are many potential opportunities for founders to attend trade shows and industry conferences in pursuit of validating the feasibility of their venture opportunity.

Technology Support

You will be surprised how your technology needs can quickly add up. Of course, many of your technology needs will be recurring expenses. But in the pre-launch phase, you tend to test various technologies to see what works for you and your team. These technologies can include platforms that support everything from project management to tracking early customer relations.

The good news is that many of these technologies provide free options with limited features or trial periods to experiment with everything the service offers. While time-consuming (and you need some discipline), taking advantage of these trial versions allows you to learn what will work best for you and your team. I constantly test out new products for my venture or support student founders.

Start by focusing on critical performance areas and outcomes that require technical support. I suggest you constantly review technology use from an internal and an external perspective. Does a particular technology help the team to manage product development more efficiently? However, does the technology also provide proper customer engagement and communication support? Most times, technologies will have internal and external-facing interfaces, so stay focused on both.

Eventually, you will find the right mix of technologies to support your business. You will incur a growing annual expense as you use these technologies more comprehensively. Many of today's products and services have recurring revenue models, and these monthly costs add up. My current technology stack costs around $2500 per year.

For many new ventures, the startup expenses can be minimal but are usually more than you first consider. Therefore, speaking with other startup founders to check some of their upfront costs is worthwhile to understand better what to expect.

Generally, I find some expenses to have well-defined, published costs. This situation is accurate for many technology platforms, government licenses & fees, and office supplies. But in many cases, founders must thoroughly investigate as costs for specific services may be less confident such as labor costs, professional services, and real estate prices. Researching similar items and services online and speaking directly to vendors and service providers to assess the actual costs is crucial.

As I have said in other writings, it is essential to institute a financial discipline during the early stages of venture development. It is a balancing act between minimizing your expenses as best you can and not taking advantage of meaningful opportunities that may make a difference in your eventual success. No matter how much effort you put into these estimates, you will want to set aside additional funds for the unexpected.

Step 3: Financial Statements

With these foundational financial model inputs, you can now go to Step 3 and build your pro forma financial statements. The business has three primary financial statements: Income Statement, Cash Flow, and Balance Sheet. Look at each role in documenting and communicating a startup's projected financial performance.

Important: I suggest that founders generate statements covering three years, month by month. However, it is best to begin by building a detailed financial model for the first 12 months. A detailed model includes the documentation of all basic assumptions and the associated estimations. Then, once you have a working model that can readily adapt to different scenarios, you can expand it to the entire 36-month period.

Income Statement

Entrepreneurs need to be able to plan operations and evaluate decisions using financial accounting information. Budgets, cash flow forecasts, and breakeven analyses are not only essential management tools, but they are also usually required information for potential investors or lenders.

Once you have completed a thorough bottom-up analysis of projected revenues and costs, you can integrate these estimations into a proforma profit and loss statement. The proforma income statement summarizes anticipated sales revenues and expenses for a specified period.

Preparing an Income Statement Forecast

There are two main objectives in generating a proforma income statement. The first reason is to project and capture performance in terms of sales, such as the percentage of increased sales or new business. Most enterprises measure success by increased customer acquisition rates and resulting sales volume. However, if the expectation is that additional sales mean higher profits, which may not always be the case, certainly increasing sales is part of the financial plan. But there is much more to it than sales performance.

The second reason for the income statement focuses on measuring profits: the difference between revenues and expenses. Sales must be profitable for the venture to succeed. A firm can determine the profitability of either products or customers. But, in the end, the enterprise must be profitable for long-term viability.

Now let's look at the critical elements of an income statement.

Revenues. Sales revenue is the total proceeds or gross income from sales to customers. Detailed statements should include the various revenue streams from individual products and service offerings.

An integral part of estimating revenue generated from each product offering is linking your sales numbers to your promotional channel strategies and calendars. You must show why these sales will occur during a particular month. This linkage is particularly crucial before having any sales history. Once you have a record of actual sales, you can begin to build estimates based on a combination of strategy and history.

Costs of Goods Sold. The following income statement line to the project is called the cost of goods sold, sometimes called direct costs. This cost area can be challenging for new venture founders to estimate. While not every product or service has a cost of goods sold component, many do. The cost of goods includes the materials and labor associated with sales from the same period. The cost of goods sold represents the resources that go into producing the products ultimately recognized as sales. These costs typically include materials, labor, and manufacturing expenses.

Costs of goods sold are a variable expense, meaning that the product cost is not accounted for until the sale transaction occurs. [Note: this is just for accounting purposes. You most likely have already paid for the labor and materials before the sale, so it still impacts your cash.] The details should include labor and associated raw materials required to produce the product. In addition, you must add shipping costs if not paid by the customer. If your business has multiple product lines, you must calculate the cost of goods sold for each product line to determine gross profit by product line. This last point is essential. I see many statements with multiple revenue-generating products recorded as one line to account for the associated costs of goods. Unless the cost of goods comprises the same components and cost amounts, this is the wrong way to present the information.

In many cases, the costs will vary based on the sales of the specific product associated with said costs. It is a best practice to monitor each product and its costs separately so you can adjust as historical performance data emerges. You can end up with a skewed view of your product costs and profit contributions each product makes.

Gross Profit. The next entry in the income statement is gross profit. This statement line should include, where possible, the gross profit by whatever categories the sales are classified (e.g., product line, geographical region). One calculates gross profit as sales less those costs of goods directly incurred to achieve the sales.

It is worth stopping for a moment to consider the importance of the gross profit line. Your gross profit numbers indicate how your products contribute to the venture's profitability. The gross profit percentage is something that you carefully monitor once you start generating sales. An important metric is also the gross profit percentage of an individual sale unit. Understanding how much a unique product contributes to profit is vital to calculating when your business will hit the all-important breakeven point. Monitoring gross profit and associated gross margin (gross profit as a revenue percentage) allows you to determine profit trends and long-term viability. As part of this analysis, you should monitor and compare margins to industry benchmarks and similar enterprises. These comparisons enable you to validate that your pricing and cost of goods sold are trending in the right direction based on your business model and overall industry performance.

Operating Expenses. This section of your income statement classifies expenses associated with your venture's operation. The costs recorded in this section are labeled indirect expenses. This statement section covers several expense categories: salaries, benefits, marketing, research and development, and computer and office supplies.

There are some standard methods to categorize and list expenses. I suggest that you work your way down from top costs down. Most startups' leading expenses will be in salaries, product development, and marketing. The remaining categories may cover general expenses such as supporting technologies and software, professional fees, insurance, co-working space costs, etc.

Like the direct expenses and resulting gross margins, you want to monitor each indirect expenditure as a percentage of total revenues. You should research industry and competitor cost percentages for pre-launch estimates for each category. For example, what is a typical percentage of salaries to revenues within your industry? These comparisons help founders evaluate if the anticipated costs align with what is going on in the marketplace. You can use this information to support your estimates and drive talent acquisition strategy and competitive salary rates. Once you start generating actual data, you can measure how your business model is working and make changes as needed.

One last area you include in the operating expense section is non-cash expenses, sometimes called intangible costs. Typically, you keep expenses like depreciation and amortization separate from tangible expenses because they do not impact your operating cash amounts. The cash outlay for these expenses happens earlier than the one you are accounting for in the current income statement. Founders can write off depreciation expenses incurred on purchasing tangible assets that the venture will use for a specific period. For example, if a founder purchases professional video production equipment for business use, a certain percentage of the cameras, screens, and lighting can be deducted as an expense for a specified period. The amount of depreciation depends on how long the equipment will last based on use and aging. One calculates the depreciation amount by dividing the asset's cost by the estimated number of years in its life minus any salvage value. Again, you want to work with your professional accountant to determine the depreciation method, time, and dollar amount. There are several depreciation methods, each having a different impact on the reporting of operating income.

You can also expense intangible assets such as specific intellectual properties such as patents, trademarks, and trade secrets. Startups can deduct the cost of these assets as expenses over several years using a process called amortization.

Operating Profit/Loss. One determines 0perating income by subtracting costs from sales, not including taxes or interest charges. Operating income is the amount the business earns after expenses but before taxes and other income, such as interest. You can refer to this as earnings before interest and taxes (EBIT). EBIT is the earnings (net income) before interest expense, interest income, and income taxes. It measures the profitability of the company's current operations as if it had no debt or investments.

EBITA. This label includes earnings before interest expense, income taxes, depreciation, and amortization. It measures the profitability of a company's operations without impacting its debt, investments, and long‐term assets. This line item allows the founder and investors to see how much cash is generated via operations but for non-operational and non-cash income and expenses.

Other Income and Expenses. This category includes interest expenses by each type of debt (e.g., leases for computers, lines of business credit, and bank loans) and other income and expenses not related to the business's everyday operations.

Pretax Income. Income before taxes is calculated by taking operating profit and factoring in other income and expenses. It denotes the income that will be subject to corporate income tax.

Income Taxes. This line item is the management's estimate of how much tax will be on its earnings. The detail should reflect amounts owed for federal and state taxes.

Net Income. This final income amount shows what earnings remain after all income and expenses and are available for dividends or reinvestment in the company.

Applications of Income Statements

The income statement is a vital tool for founders and investors to evaluate overall business profitability and analyze the impact of specific business activities. Here are some key ways to apply the income statement insights:

Evaluate product/service profitability - By analyzing gross profit after deducting the costs of goods sold from revenues; founders can see which offerings are most profitable. This approach helps determine which products to prioritize or if pricing needs adjustment.

Assess operational efficiency - Looking at operating expenses as a percentage of revenues shows how efficiently the business is running. Founders can identify expense areas needing reduction or gaps requiring investment.

Understand tax implications - Modeling different revenue growth and expense reduction scenarios will demonstrate how taxes influence net income. Founders can look for ways to minimize tax liability.

Communicate with stakeholders - The income statement helps convey the business case to investors, lenders, and shareholders. Founders can clearly show the potential for profitability and growth.

Monitor performance - Comparing actual income statements to projections enables continuous improvement. Founders can pinpoint variances, course correct, and refine predictions.

Evaluate business model - A well-constructed income statement allows a comprehensive assessment of whether all pieces of the business model integrate to drive profitability.

In summary, the income statement is a multifaceted tool to assess the past and plan the future. When crafted appropriately and monitored regularly, it provides invaluable visibility into the financial inner workings of a startup.

Cash Flow Statements

An income statement may show that the company is profitable over a given period but does not give any information about the cash position. A seemingly profitable venture can go bankrupt if its short‐term cash position is insufficient to meet its short‐term liabilities, such as salaries, interest payments, and other receivables. This situation is particularly true with early‐stage companies, which, more often than not, are cash-strapped. Therefore, this statement and its use to predict cash availability to pay bills are the most important for the entrepreneur to understand and use. It is advisable to have a month‐by‐month cash flow forecast for the company's first two to three years, as cash reserves will fluctuate wildly.

Preparing a Cash Flow Forecast

Reasons to Prepare a Cash Flow Forecast. Keeping close tabs on required and available cash is the most crucial estimate an early-stage enterprise can monitor. While correct revenue recognition is essential for a compliant profit and loss statement, cash flow is much more critical to operations. For early estimates, month-by-month budgeting is the best approach. Businesses almost always incur costs, while revenues are less reliable. Knowing your cash position helps determine the amount, timing, and disbursement schedule of financing you will need to continue operations before becoming self-sustaining.

A cash flow forecast shows the amount of cash (receivables) and money going out (payables) during a particular month. The forecast also indicates to a bank loan officer (or the entrepreneur) what additional working capital the business may need, if any. In addition, it provides evidence that there will be sufficient COH to make the interest payments on a revolving line of credit or to cover the shortfalls when payables exceed receivables.

Cash flow statements use information from both the income statement and balance sheet (see below). Your account explains changes in cash flows resulting from business operations and financing activities. The reconciliation section of the cash flow worksheet begins by showing the balance carried over from the previous month's operations. Next, one adds the net inflows/outflows or the current month's receipts and disbursements. This adjusted balance will be carried forward to the first line of the reconciliation portion of the following month's entry to become the base to which the next month's cash flow activity will be added or subtracted.

Modifications to sash flow statements occur as new things are learned about the business and paying vendors. You should compare the cash flow forecast to each month's projected figures with each month's actual performance figures. Having a second column for the actual performance figures alongside each " planned " column in the cash flow worksheet will be helpful. Look for significant discrepancies between the planned and actual figures.

Founders and investors pay close attention to cash flow management and performance. One of the critical metrics that startups should monitor closely is what is commonly called the burn rate. The burn rate is when a new venture uses up its cash to finance overhead before generating positive cash flow from operations. In other words, it's a measure of negative cash flow. The burn rate is cash spent per month. The burn rate is determined by looking at the cash flow statement. The cash flow statement reports the firm's cash position change from one period to the next by accounting for the cash flows from operations, investment, and financing activities. Compared to the amount of cash a company has, the burn rate gives investors a sense of how much time is left before the company runs out of money— sometimes called your runway.

As part of a founder's financial discipline, you should monitor your venture's cash position daily. I would make this information, along with metrics such as burn rate, runway, and breakeven, a significant part of a performance dashboard.

Balance Sheet

The balance sheet provides a picture of the business's financial position at a particular point in time—generally at the end of a financial period (e.g., month, quarter, or year). It encompasses everything the company owns (assets) or owes (liabilities), as well as the investments into the company by its owners and the accumulated earnings or losses of the company (equity). The balance sheet equation is assets=liabilities+shareholder equity. Investors and banks commonly analyze various assets and liabilities ratios on the balance sheet to determine a venture's viability.

Preparing a Balance Sheet Forecast

On the balance sheet, one divides assets into short and long-term categories. Current assets are converted into cash within one year. These assets include the current cash balance (from cash flow), payments due from customer sales (accounts receivable, and inventory. You will consider inventory a current asset if sold within one year from receipt; however, specific business inventories can be further segregated into work‐in‐process (WIP), raw materials, or finished goods inventories.

Tangible and intangible long-term assets include items such as buildings, vehicles, computer equipment, and intellectual property forms. Record these assets at their original cost minus any accumulated depreciation as expenses in the current income statement.

On the other side of the balance sheet equation, you have the liabilities and shareholders' (stockholders') equity sections. Liabilities consist of any amounts the company owes creditors. Similarly, liabilities are current if you pay them within one year; otherwise, they are considered long‐term. Short-term liabilities include interest payments on loans recorded in the income statement and any payments you owe suppliers (accounts payable). Longer-term liabilities are typically balances on loans linked to long-term assets, such as mortgages on a building or lease payments for a company vehicle.

The difference between the total assets and total liabilities is called stockholders equity. Much like an individual, the number is considered the net worth of the venture. This number comprises any stock issued by the company and accumulated earnings retained throughout the years, as shown in profits from the income statement.

When analyzing a company's balance sheet, managers and investors view it in terms of its type of business. For example, fixed assets account for a more significant percentage of total assets in a manufacturing operation than a distributor or professional services company. Therefore, analyze the balance sheet with the volume of the company's business in mind. For instance, one compares receivables to sales to determine how quickly the company collects its cash or current liabilities compared to expenses to see if it pays its short‐term obligations promptly.

Bringing It All Together

While each of these statements is a separate document, several linkages exist. For example, select information from cash flow analysis links to the balance sheet, such as net increase or decrease in cash as demonstrated in the case analysis, will be reflected in the cash asset column in the balance sheet. Any cash outlay for an asset will be in both statements. Net income from the profit and loss statement will impact the balance sheet's cash flow and retained earnings. As founders and investors analyze a venture's performance, it is essential to review these statements together, not in isolation.

A Note on Financial Templates

In general, I am not a fan of pre-determined financial templates. While they can be helpful as a starting point, no template covers the assumptions and estimates particular to your business model. If you use a template with pre-existing formulas, ensure you can readily adjust any parts of the statements, labeling line items and assumptions. However, I think it is worth your time to start with a blank slate, using one of the standard computer spreadsheet programs such as Microsoft Excel or any full‐faceted business software to generate your financial statements. If you plan to start with an existing template, you should look for templates that best fit your business model and overall financial planning approach. For example, not all templates provide 36-month-by-month entry capability. Many template designs annualized performance over a 3-5 year period. Does the template include the three statements with proper integration embedded in the model? Some templates provide several analysis tools and metrics based on the inputs into the statements. Such analytics as breakeven, customer acquisition costs, and monthly recurring revenue are vital data points for startups. For customer acquisition and revenue modeling, does the template provide the capability for multi-tier pricing, retention, and churn rates? Finally, how does it support assumption documentation, different currencies, performance graphics, and data uploads or downloads? Sometimes you can find templates designed for a specific industry (Hospitality) or product category (SAAS).

Template pricing models include free downloads, trial periods, one-time fees, and recurring costs for online systems. The good news is that there are plenty of options. All that said, you may want to check out some of the samples from my startup resource database.

Conclusion

Creating startup financial statements is an invaluable exercise for founders. Though projections rely on assumptions without actual data, the process requires methodically thinking through all business model elements and how they integrate. Revenue models, cost structure, resource needs, cash availability, and profit potential interrelate in the viability equation. Crafting these projections gives founders their first quantified view of the business case to evaluate, communicate, and track.

While theory and estimation generate the initial statements, customer feedback and real-world performance will enable refinement. The success mindset embraces financial projections as living documents to adjust. As operations commence, compare actuals to forecasts to pinpoint variances and enhance predictive capability. With a dedication to financial rigor in the earliest stages, founders put themselves in the best position to activate their business models and realize their entrepreneurial dreams.

Keep reading with a 7-day free trial

Subscribe to Innovate & Thrive to keep reading this post and get 7 days of free access to the full post archives.